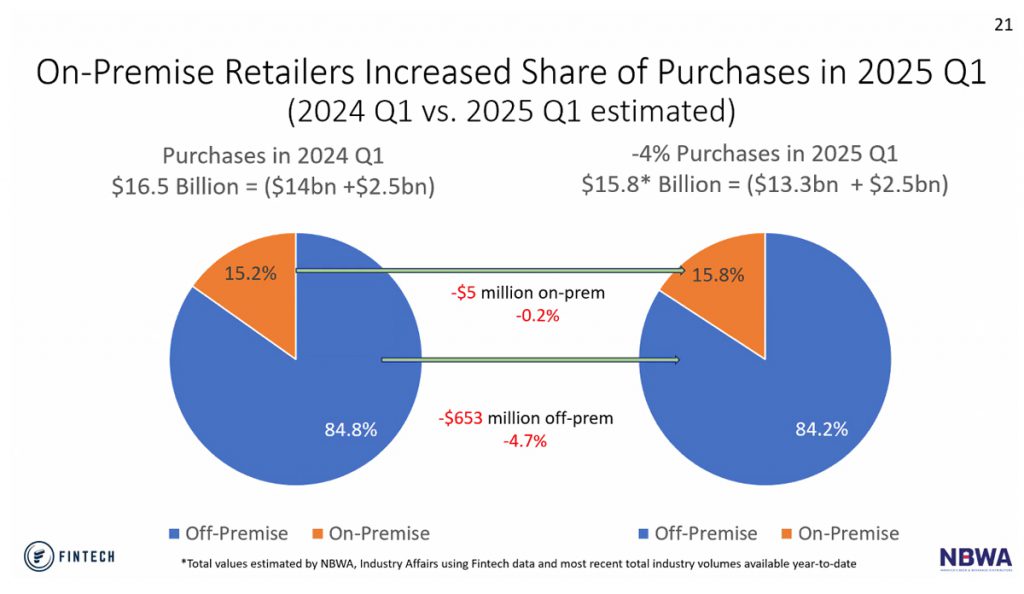

Overall beer category dollar sales declined in Q1 2025 compared to Q1 2024, but those losses were unbalanced between the channels, according to the most recent report from the National Beer Wholesalers Association (NBWA) and Fintech.

Beer dollar sales reached an estimated $15.8 billion in the first quarter of the year, down about 4% year-over-year (YoY). But on-premise dollar sales declined just 0.2% – nearly flat – compared to the off-premise’s 4.7% decline.

“Indeed, it is not the best of times that we’ve seen in many of our previous slides where we’ve been able to deliver some bad news, but lots of good news,” NBWA chief economist and VP of analytics Lester Jones said.

Jones kicked off the quarterly webinar by likening the beer industry to Mike Myers’ titular character in Austin Powers: International Man of Mystery, who has lost his mojo. Unfortunately for beer, the solution won’t be as easy as storming Dr. Evil’s lair, as there are likely several culprits afoot.

“I haven’t figured out statistically and quantitatively what the main drivers are, but I do know it’s a bunch of things,” Jones said. “It’s not just one-to-one. It’s one-to-many for the beer industry.”

Off-Premise Weakness, Retail Accounts Flat Post-Pandemic

On-premise business remaining nearly flat could not offset the off-premise channel’s weakness, as the on-premise accounted for 15.8% of all beer category dollar sales, compared to 84.2% in the off-premise.

Recovery in the beer-selling retail trade seems to have stalled post-COVID-19 pandemic, with retail accounts flat to 2024 with 252 retailers per capita. Beer retailers per capita peaked at 269 per capita in 2017, which was “the ultimate just craziness of putting beer wherever we think it should go, where it doesn’t necessarily belong,” Jones said.

That number landed at 260 in 2019 and plummeted to 242 in 2020.

“What we saw coming out of COVID was consistent growth year-over-year in the number of beer retail accounts,” Jones said. “2025 just doesn’t seem to have the mojo to keep that trend up.”

About 70% of all new beer-selling accounts in Q1 were on-premise, which accounts for a far smaller ratio of sales than the off-premise.

“People need to recognize that the bulk of our accounts are coming in the on-premise, and we’ll see that in the data,” Jones said.

During Q1, both cans and kegs gained share in the off- and on-premise, respectively. Cans’ share of off-premise dollar sales reached 69.2% (up 0.8% YoY), while bottles accounted for 30.7% and kegs were 0.2%.

In on-premise accounts, kegs gained 4% share from packaged offerings, bringing draft’s share of invoice dollars to 55.5%. Both bottles (25.9%, -2.5% YoY) and cans (18,6%, -1.5% YoY) lost share.

Demographic Defense

The share of 21- to 24-year-olds who have drunk beer in the past 30 days has reached its lowest point the past decade, with only slightly more than 30% of the youngest legal drinking age (LDA) adults reporting consuming the product, according to Scarborough USA data cited by Jones.

The last time the share of younger LDA, recent beer drinkers was this low was in 2013, when it dipped to slightly less than 25%.

“Their share is dropping off – that’s a big problem for us as an industry and as a category,” Jones said. “We’ve got to tag the 21- to 24-year-olds and bring those up.”

Ratings of televised sports – historically beer-drinking occasions – have been “soft,” Jones pointed out, but added that legalized sports betting shows that consumers are still interested in sports.

“Sports betting continues to grow,” he said. “Where those dollars go from, I don’t know.”

“It’s a lot of the LDA 21-34 males, who we need drinking beer,” webinar co-host and Fintech VP of distributor strategy Eric Kiser added.

Segment and Supplier Share Shifts

Editor’s note: Fintech data represents about one-third of all alcohol sales from wholesalers to retailers. It includes more than 1 million weekly invoices from 5,296 distributors and 257,929 retailers nationwide.

Premium plus lights held the largest share in both the off-premise (30.1%, -0.1% YoY) and on-premise (42.5%, +0.3% YoY).

Imports, the No. 2 segment, were the largest share gainer across both channels, increasing off-premise share 0.8%, to 23.9%, and on-premise share 0.6%, to 24%.

Craft beer was the biggest share donor, losing 0.8% share points in both the off-premise, where it accounted for 10.1% of dollars, and on-premise (17.3% share). Beyond beer (malt-based hard seltzers and flavored malt beverages) was the second largest share loser and also lost share across both channels, down 0.6% YoY, to 14.7% in the off-premise; and down 0.7% YoY, to 3.5% in the on-premise.

In addition to craft and beyond beer, below premium regular and cider both lost 0.1% share in both the off-premise and on-premise. Below premium regular accounted for 6.2% in the off-premise and 1.2% in the on-premise, while cider held a 1% share in the off-premise and 1.4% in the on-premise.

Below premium light was flat in the off-premise (6.2% share), but gained 0.3% share in the on-premise, where it accounted for 3.1% of dollars.

Additional on-premise share gainers include:

- Premium plus regular, +0.1% YoY, to 5.3%;

- Non-alcoholic (NA) beer, +0.2% YoY, to 1.1%;

- And all other styles, +0.2% YoY, to 0.6%.

Other segments gaining share in the off-premise include:

- Premium plus regular, +0.2% YoY, to 8.2%;

- NA beer, +0.4% YoY, to 1.7%;

- And all other styles, +0.3% YoY, to 1.2%.

Only three of the top 10 suppliers gained share in the off-premise during Q1:

- No. 1 Anheuser-Busch (A-B) InBev, +0.2% YoY, to 31.5%;

- No. 3 Constellation Brands, +0.9% YoY, to 17.6%;

- And No. 7 Diageo, +0.1% YoY, to 2%.

Three were flat – No. 4 Mark Anthony Brands (6.2% share), No. 9 New Belgium (1.6% share) and No. 10 Pabst (1%).

Four of the top 10 suppliers lost share in the off-premise during Q1:

- No. 2 Molson Coors, -0.4% YoY, to 31.5%;

- No. 5 Boston Beer, -0.2% YoY, to 4.3%;

- No. 6 Heineken, -0.1% YoY, to 3.7%;

- No. 8 Yuengling, -0.1% YoY, to 1.6%.

All other suppliers also lost 0.4% share YoY, to 11.7%. All other suppliers gained share in the on-premise during the quarter, increasing 0.6%, to 10.8% share.

No. 1 A-B was the largest share gainer among the top 10 suppliers in the on-premise. Its share jumped 0.9% YoY, to 34.1%, followed by No. 3 Constellation (+0.6% YoY, 12.8% share), No. 5 Yuengling (+0.2% YoY, 2.9% share) and No. 7 Diageo (+0.4% YoY, 2.2% share).

Six of the top 10 suppliers lost share in the on-premise in Q1:

- No. 2 Molson Coors, -0.4% YoY, to 25.9%;

- No. 4 Heineken, -0.3% YoY, to 4.9%;

- No. 5 (tied with Yuengling) Boston Beer, -0.2% YoY, to 2.9%;

- No. 8 New Belgium, -0.2% YoY, to 1.9%;

- No. 9 Mark Anthony Brands, -0.3% YoY, to 1.6%;

- No. 10 Pabst -0.2% YoY, to 1%.

At the brand level, A-B’s Michelob Ultra had the largest share both off-premise (9.2%) and on-premise (14.9%) and the greatest share gains in both (+0.9% and +1.4%, respectively).

A-B held four of the top 10 brands across both channels. No. 3 Bud Light lost share both off-premise (-0.6% YoY, to 7.2%) and on-premise (-0.7%, to 7.4%), while No. 8 Budweiser’s share declined 0.2% in each channel, bringing the brand’s share to 3.4% off-premise and 1.7% on-premise. No. 9 Busch Light gained 0.3% share in both channels, bringing its share to 3.3% off-premise and 2.3% on-premise.

Following Michelob Ultra, No. 2 Constellation’s Modelo Especial was the next largest share gainer, increasing 0.5% off-premise, to 8.7%, and 0.8% on-premise, to 7.1%.

No. 5 Constellation’s Corona Extra was the only other brand to gain share, +0.2% off-premise, to 5.1%. Its on-premise share declined 0.4%, to 3.1%.

No. 7 Mark Anthony’s White Claw declined 0.1% off-premise, to 3.5% share, and 0.2% on-premise, to 1.5%.

All other brands lost more share off-premise than any of the top 10, dropping 0.9% to 44.9%. All others dropped 0.6% in the on-premise, to 42.4% share.

Molson Coors’ core premium light brands, Miller Lite and Coors Light, tied at No. 4 in off-premise with 6.2% share; both shed 0.2% share in Q1. In the on-premise, No. 4 Miller Lite pulled away from its sibling with 10% (-0.4% YoY) share. No. 5 Coors Light accounted for 9.1% share on-premise (-0.1% YoY).

No. 10 Boston Beer’s Twisted Tea gained 0.1% share in the off-premise, bringing its share to 2.3%, but lost 0.1% in the on-premise (0.5% share).

Drifting Draft Shares

Only nine of the top 29 draft brands managed to gain share in the on-premise during Q1:

- No. 1 Michelob Ultra, +1.4% YoY, to 15.7%;

- No. 4 Modelo Especial, +1.3% YoY, to 8.3%;

- No. 10 Diageo’s Guinness, +0.5% YoY, to 2.6%;

- No. 12 Busch Light, +0.3% YoY, to 1.7%;

- No. 13 Constellation’s Pacifico, +0.3% YoY, to 1.6%;

- No. 14 A-B’s Kona, +0.2% YoY, to 1.4%;

- No. 20 A-B’s Golden Road, +0.2% YoY, to 0.8%;

- No. 26 Molson Coors’ Coors, +0.1% YoY, to 0.5%;

- No. 29 Constellation’s Modelo Negra, +0.2% YoY, to 0.4%.

No. 5 Bud Light was the largest share loser, declining 1.1%, to 8.1%, followed by No. 6 Molson Coors’ Blue Moon (-0.6% YoY, to 7.5%), No. 2 Miller Lite (-0.5% YoY, to 10.4%), No. 7 Heineken-owned Dos Equis (-0.4%, to 4.3%), No. 9 A-B’s Stella Artois (-0.2% YoY, to 3.7%), No. 11 Boston Beer’s Samuel Adams (-0.2% YoY, to 1.9%), No. 16 New Belgium-owned Bell’s (-0.2% YoY, to 1.1%), No. 3 Coors Light (-0.1% YoY, to 9.6%), No. 19 Budweiser (-0.1% YoY, to 0.9%), No. 21 A-B’s Goose Island (-0.1% YoY, to 0.7%) and No. 27 New Belgium’s Voodoo Ranger (-0.1% YoY, to 0.4%).

Share for nine of the top 29 draft brands was flat in Q1:

- No. 8 Yuengling, 4.1% share;

- No. 15 Sierra Nevada, 1.1% share;

- No. 17 (tie) New Belgium (Voodoo Ranger excluded), 1% share;

- No. 17 (tie) Gambrinus’ Shiner, 1% share;

- No. 22 (tie)Boston Beer’s Angry Orchard, 0.6% share;

- No. 22 (tie) A-B’s Elysian, 0.6% share

- No. 22 (tie) Duvel’s Firestone Walker, 0.6% share;

- No. 25 Pabst, 0.5% share;

- No. 27 Heineken, 0.4% share.

Other draft highlights include:

- In California, No. 1 draft beer Modelo Especial outsells its next largest competitor, No. 2 Michelob Ultra, by 300%.

- But in Texas, Modelo is a distant No. 3 and 200% outsold by No. 2 Dos Equis.

- Coors Light is No. 1 on draft in Washington state, and outsells No. 2 Modelo by 2.5X.

- However, in Illinois, there are no similarly wild dollar share gaps, as the top five brands (Miller Lite, Modelo, Yuengling, Guinness and Blue Moon) are separated by just $500,000 in sales.

Editor’s note: Look for further coverage from the webinar later this week.