Wholesalers purchased fewer cases and kegs in nearly every segment of the beer category in April, according to the most recent Beer Purchasers’ Index (BPI) from the National Beer Wholesalers Association (NBWA).

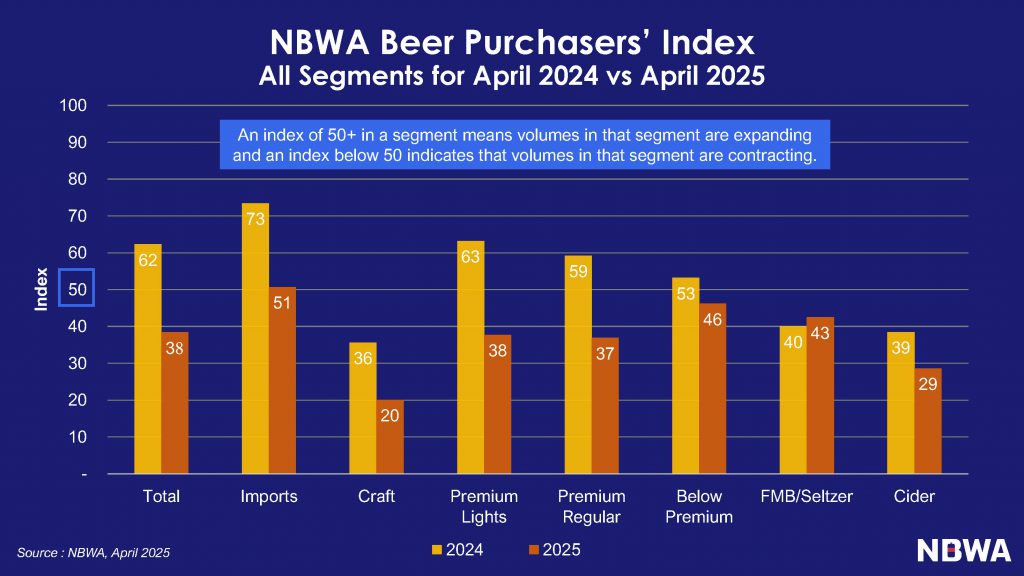

Total beer and every segment except for imports were in contraction. The overall category registered a reading of 38 for the month. Anything less than 50 indicates a segment is contracting, while over 50 means expansion.

At-risk inventory – product in warehouses within 30 days of its expiration date – increased 4 points from March 2025, to 54.

“The combination of these index readings continues to place the industry in contractionary territory,” NBWA chief economist and VP of analytics Lester Jones wrote.

Imports recorded an index of 51, which marked a 22-point year-over-year (YoY) decline from April 2024. The segment was in contraction last month for the first time since April 2020.

Although still in contraction, flavored malt beverages (FMB) and hard seltzer were the only segment to record YoY growth, increasing 3 points to 43.

“FMB/Seltzer recorded its 14th consecutive month of YoY improvement — the segment’s first such streak since 2019/2020,” Jones wrote.

Below premium recorded the smallest YoY drop, declining 7 points to 46, followed by cider, which fell 10 points to a reading of 29.

Premium light recorded a 25-point YoY drop, to 38, a far cry from April 2024, when the segment was well in expansion as it cycled the one-year anniversary of the conservative-led Bud Light boycott.

Premium regular followed a similar trajectory, declining more than 20 points YoY to 37 in April 2025.

Craft posted the lowest reading (20) for another consecutive month, though craft’s reading remained flat month-over-month. Jones pointed out that flagging distributor interest may not indicate as much of a segment health as it seems.

“I don’t see craft consistently below 50 as much as a consumer demand problem as it is a craft over-supply problem,” he told Brewbound. “Retailers have constraints on how much product they can physically put on shelves.”

Of the 9,612 craft breweries in operation last year, 2,200 sell their beer primarily through distribution, according to the Brewers Association’s (BA) annual craft production report, which was released last month. There were about 3,000 beer distributors in operation in 2020, according to the NBWA’s website. The middle tier has continued to consolidate since then, creating a bottleneck for smaller craft breweries.

“There’s only so many shelf sets and distributor trucks,” BA president and CEO Bart Watson told members of the media Thursday during the Craft Brewers Conference. “There’s only so many brands that could succeed. I would separate that somewhat from the total number of breweries. Could we see a world in which there are a lot fewer brands that are going out in broad distribution to the supermarkets in the next five, seven years, but that the total brewery number is roughly similar? I think that’s a possibility.”

Craft’s reliance on IPAs may have created fatigue across the three tiers. The style accounted for 54% of craft dollars and 51% of craft volume year-to-date (YTD) through March 23 at off-premise retailers tracked by market research firm Circana. While IPA is far from monolithic, the nuances of its sub-styles may be lost on consumers, who also have more bev-alc choices than ever before across beer, wine and spirits.

“Craft has the long tail that is getting cut by retailers. I would bet that most ‘normal’ consumers don’t notice less IPA choices on the shelves,” Jones said. “Meanwhile, the innovation machine continues to go full steam ahead in 2025 with tremendous choices among all the liquid refreshment segments.”

Jones likened craft’s current conundrum to a chicken-or-the-egg situation.

“If you think about each segment in the beer industry, craft is the most fragmented in terms of supplier, brands, and products,” he said. “It is the one segment that has the most to give back in a crowded and oversupplied market. As retailers are buying less craft from distributors, beer distributors are ordering less from craft brewers.”

Of the major segments within the beer category, only domestic premium outpaced craft’s losses in dollars (-6.1% for domestic premium, -4.5% for craft) and volume (-7.3% for domestic premium, -5.7% for craft) YTD through March 23, according to Circana.