Editor’s Note: This story first appeared in the November/December issue of BevNET Magazine. It has been adjusted slightly with updated data and current events.

For most folks, October is the time to bring old sweaters out of storage, indulge in pumpkin-flavored everything and grab a last-minute Halloween costume. For Schilling Hard Cider, October is its Super Bowl.

Seattle-based Schilling is the leading cidery behind National Cider Month (NCM), a brand-agnostic campaign to promote the hard cider segment with demonstrations, retail activations and digital marketing.

More than 150 cideries participated in NCM in 2024 – up from 60 in 2023 – and more than 300 events and in-store demonstrations were held, Schilling CMO Rachel Thomas told Brewbound. And those figures only include folks that submitted events and campaigns to the official NCM website, a one-stop shop for NCM assets, hard cider educational resources and event listings.

Several trade groups also participated last year, including the U.S. Apple Association, American Cider Association (ACA), Cider Institute of North America, Iowa Brewers Guild, Michigan CIder Association, Minnesota Cider Guild, Northwest Cider Association, Pennsylvania Cider Guild and the Utah Cider Association.

“There’s just more buy-in this year overall,” Schilling CCO Eric Phillips told Brewbound. “There was more awareness about it, there was more participation overall, there was more excitement, there was more enthusiasm.”

2024 marked Year 5 of NCM (previously National Apple Month), but only its second year as a national campaign with programming across the U.S.

“Last year was, ‘Let’s start it. Let’s learn about it as it goes national,’” Phillips said. “This year was, ‘OK, let’s go a little bit further.’”

In 2023, Whole Foods became a prominent retail partner for NCM, joining after a conversation between Mary Guiver, Whole Foods global principal category merchant for beer, and Schilling leadership at the 2022 Brewbound Live business conference. The grocery chain partners with local and regional cider brands on displays and placements.

Now, NCM has garnered enough traction and created enough growth for the segment, that other retailers and major distributors are carving out space for NCM in their annual business plans.

“You’re talking about Columbia, Reyes, Hayden, Crescent Crown, Coors Distributing,” Phillips said. “You’re talking about some heavy hitters who are already earmarking it for next year.”

Schilling Cider is the driving force behind NCM, but the company insists that the campaign is brand-agnostic, and meant to help build greater awareness for the total hard cider segment, whether it’s limited-release bottled farm ciders, or nationally available brands.

“We have an opportunity as stewards in the industry specific to cider to help foster a community of growth,” Phillips said. “We can’t grow a category solo, we need other people.

“We’re at this point where it’s like, ‘Hey, I promise there’s not like, some secret, dark thing that we’re trying to do on the back end, like we’re not puppeting,’” he continued. “We are trying to help you grow your site or share as well in your market. Here are some tools, and here is a nationally designated program that can do that.”

Still, Schilling’s efforts aren’t completely selfless. The company recorded its “best month ever” in October, increasing dollar sales +24% versus October 2023, which was its previous best month. More than 20 major retailers increased their Schilling sales during NCM versus year-to-date (YTD) trends, and California became the company’s fastest-growing market, increasing dollar sales +74%, thanks in part to support from Schilling’s distributor partner Reyes, according to Phillips.

NCM efforts come as hard cider finds itself in a time of transition. The segment was long dominated by national players such as Boston Beer Company’s Angry Orchard, still the No. 1 shareholder. National brand declines dragged down the overall segment trends, creating the perception that hard cider couldn’t grow and connect with consumers. But behind the scenes, regional cideries were finding opportunities and working to eliminate hard cider stereotypes with consumers. Two years ago, regional cideries passed national cider brands for more than 50% share of the segment.

Hard cider is still recording losses, impacted by continued declines by major brands, including Vintage Wine Estates’ Ace Cider, which recently filed for Chapter 11 bankruptcy and was sold at auction. Hard cider dollar sales declined -2.1% and volume -4.1% in NIQ-tracked off-premise channels in 2024, according to data shared by 3 Tier Beverages (ending December 28).

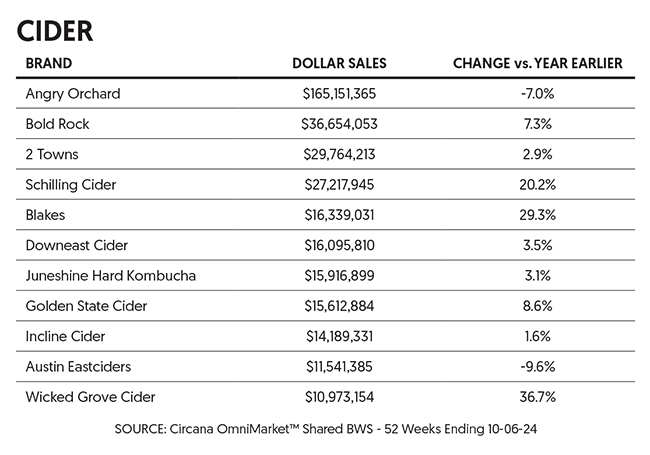

However, the data looks much rosier when looking at regional trends, especially with the NCM boost. Eight of the top 10 cider suppliers increased dollar sales growth in Circana-tracked off-premise channels in the four-week period ending October 27, according to data shared by Schilling. Total cider dollar sales also increased +20% in the four-week period versus summer trends.

Additionally, hard cider is looking to capitalize on new standards of fill allowances to grow the segment. The Alcohol and Tobacco Tax and Trade Bureau (TTB) approved 13 new standards of fill for wine, hard cider and mead producers this month, including 16 and 19.2 oz. packages, allowing producers to participate in the popular formats with offerings 7% ABV and above.

This is the second expansion of standards of fill for wine, hard cider and mead in a four-year period. In December 2020, the TTB added allowances for 355 ml (12 oz.), 250 ml (8.45 oz.) and 200 ml (6.76 oz.). At the time of the change, hard cider had 0.8% share of total beer category dollar sales, according to previous reporting. As of December 28, 2024, the segment has grown \to 1.1% share in NIQ-tracked off-premise channels.

“It’s a category that’s poised for growth, it just happens to be cider, right?” Phillips said. “The conversation with our distributor partners is, ‘What are people looking for?’ People are looking for flavor, and then people are looking at high ABV – those are two of the top determining factors if you’re going to purchase, and cider has that space.”

A continued hurdle within the segment is “a gap in quality” among offerings, though that is changing, Phillips said. That’s not just regional cidery efforts, but also Angry Orchard reformulating its core offerings.

Additionally, the segment is still burdened by consumer education. It takes work to show how many different brands of hard cider are available in the market, or what different styles of hard cider there are, including the difference between semi-sweet, semi-dry and dry cider, according to Thomas.

“Just by putting that on the can, it starts the conversation of, ‘Oh, this is what a dry cider is,’” she said.

Brewbound senior reporter Zoe Licata will travel to Chicago next week for CiderCon (February 5-7), the ACA’s annual industry conference. Look for more hard cider coverage in the coming weeks.

Looking to catch up on cider-related news before the event? Check out some of our previous coverage:

- Former Dairy Farmers of America Exec to Lead American Cider Association

- New York Governor Passes DTC for Hard Cider and Spirits

- A Round With Yonder Cider Founder and CEO Caitlin Braam

- Ryan Burk Joins Blake’s Beverage as VP of Quality & Innovation

- Stormalong Founder Reflects on 10 Years of Respecting the Apples

- Brewbound Live: The Strength of Regional Cideries and Breaking the Myth that Cider’s Failing